Why Conventional Mortgage Loans Are a Smart Selection for Stable Financing

Why Conventional Mortgage Loans Are a Smart Selection for Stable Financing

Blog Article

Understanding the Numerous Sorts Of Home Loan Offered for First-Time Homebuyers and Their Special Benefits

Navigating the range of home mortgage lending options available to first-time buyers is important for making informed monetary choices. Each kind of finance, from standard to FHA, VA, and USDA, presents distinct advantages customized to diverse purchaser demands and conditions.

Standard Lendings

Traditional fundings are a foundation of mortgage funding for first-time homebuyers, giving a dependable option for those aiming to acquire a home. These financings are not insured or guaranteed by the federal government, which identifies them from government-backed car loans. Normally, standard car loans call for a greater credit history and a more substantial down settlement, commonly varying from 3% to 20% of the purchase price, depending on the lending institution's requirements.

One of the significant advantages of traditional lendings is their flexibility. Consumers can select from different car loan terms-- most generally 15 or three decades-- enabling them to straighten their home mortgage with their financial objectives. In addition, traditional lendings may provide reduced rate of interest contrasted to FHA or VA lendings, especially for consumers with strong credit rating accounts.

An additional benefit is the lack of ahead of time home loan insurance costs, which are usual with government finances. However, personal home loan insurance policy (PMI) might be called for if the deposit is much less than 20%, but it can be removed once the consumer achieves 20% equity in the home. In general, standard car loans provide a practical and attractive financing choice for first-time homebuyers looking for to navigate the mortgage landscape.

FHA Lendings

For numerous newbie buyers, FHA financings represent an obtainable pathway to homeownership. One of the standout attributes of FHA lendings is their low down payment requirement, which can be as low as 3.5% of the purchase price.

Furthermore, FHA lendings enable greater debt-to-income ratios contrasted to standard loans, accommodating customers that might have existing financial obligations. The passion rates connected with FHA fundings are often affordable, further improving price. Customers additionally take advantage of the capacity to consist of particular closing costs in the loan, which can reduce the in advance financial problem.

Nonetheless, it is necessary to note that FHA financings need home mortgage insurance costs, which can raise monthly repayments. Regardless of this, the overall benefits of FHA financings, including access and reduced initial prices, make them an engaging alternative for new buyers seeking to go into the property market. Comprehending these car loans is important in making notified decisions regarding home financing.

VA Loans

VA loans use an unique funding option for qualified veterans, active-duty solution participants, and specific participants of the National Guard and Books. These lendings, backed by the U.S - Conventional mortgage loans. Department of Veterans Matters, offer numerous advantages that make home possession much more easily accessible for those that have served the country

Among the most substantial benefits of VA fundings is the absence of a deposit requirement, enabling qualified borrowers to fund 100% of their home's purchase rate. This function is specifically helpful for new property buyers who might struggle to conserve for a substantial deposit. In addition, VA lendings generally come with affordable rate of interest, which can cause lower month-to-month repayments over the life of the financing.

Another remarkable benefit is the lack of personal home mortgage insurance policy (PMI), which go right here is frequently needed on traditional finances with low down payments. This exemption can lead to considerable financial savings, making homeownership more cost effective. VA financings offer versatile debt demands, allowing borrowers with reduced credit score ratings to qualify more quickly.

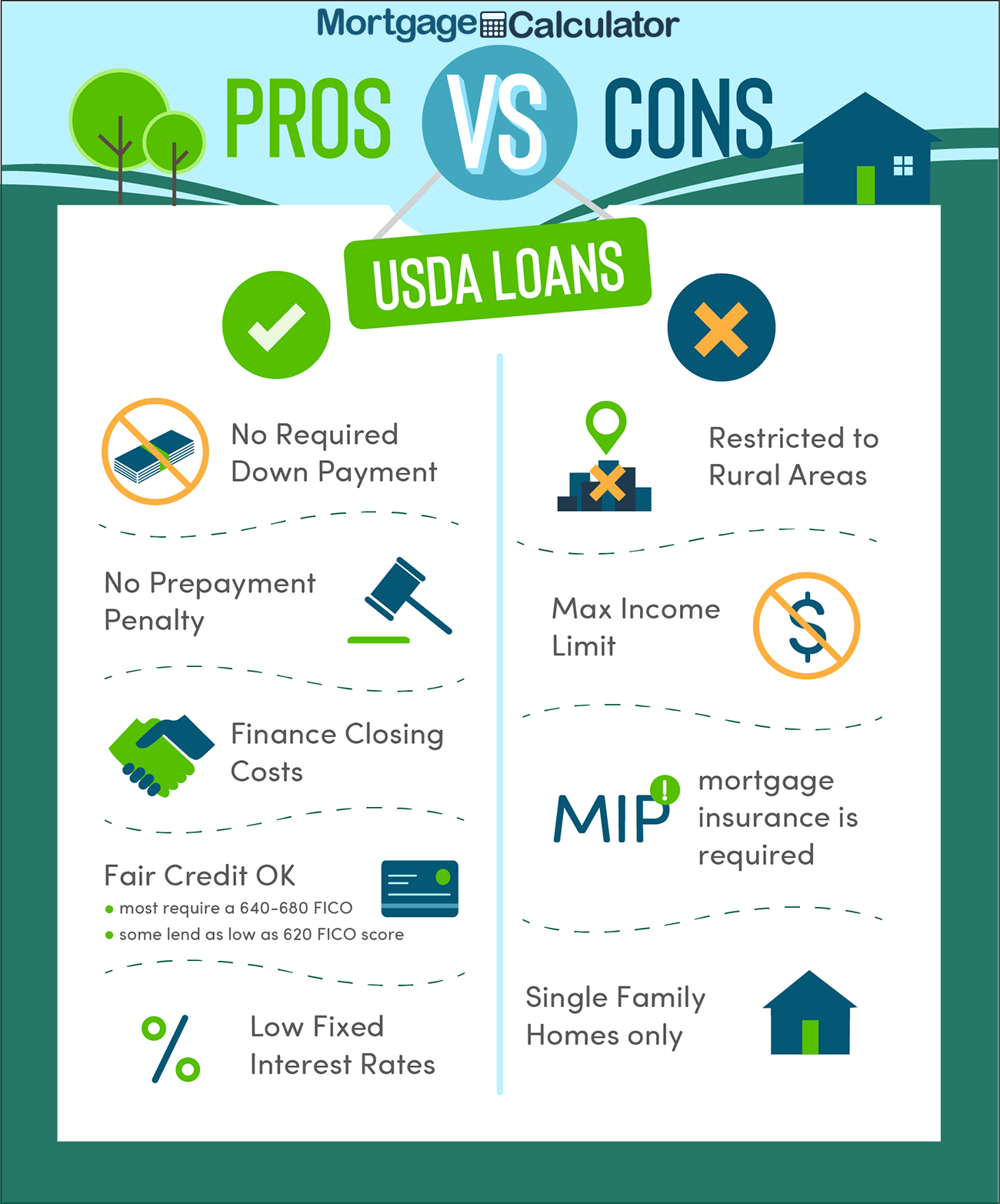

USDA Lendings

Discovering financing options, novice property buyers might find USDA finances to be an engaging choice, especially for those seeking to buy residential or commercial property in country or rural areas. The USA Division of Farming (USDA) supplies these loans to promote homeownership in designated rural regions, providing an exceptional opportunity for qualified customers.

One of the standout features of USDA financings is that they require no down payment, making it less complicated for new purchasers to go into the real estate market. Furthermore, these car loans generally have affordable rates of interest, which can lead to reduce monthly repayments contrasted to traditional funding alternatives.

USDA finances also include flexible credit history needs, allowing those with less-than-perfect credit score to certify. The program's income limits make sure that assistance is directed towards low to moderate-income households, better sustaining homeownership objectives in rural areas.

Furthermore, USDA fundings are backed by the federal government, which lowers the threat for lending institutions and can improve the authorization procedure for debtors (Conventional mortgage loans). As an outcome, new buyers thinking about a USDA car loan might locate it to be a useful and easily accessible alternative for achieving their homeownership dreams

Unique Programs for First-Time Buyers

Numerous new property buyers can take advantage of unique programs made to help them in navigating the intricacies of buying their very first home. These programs frequently offer financial motivations, education, and sources customized to the special requirements of newbie buyers.

Furthermore, the HomeReady and Home Feasible programs by Fannie Mae and Freddie Mac provide to reduced to moderate-income purchasers, using flexible mortgage options with try this out reduced home mortgage insurance policy costs.

Educational workshops hosted by different organizations can likewise help first-time customers comprehend the home-buying procedure, enhancing their chances of success. These programs not just ease financial problems but likewise encourage helpful hints buyers with understanding, inevitably assisting in a smoother change right into homeownership. By checking out these unique programs, first-time property buyers can discover useful sources that make the desire of possessing a home much more attainable.

Verdict

Conventional financings are a cornerstone of home mortgage financing for newbie buyers, giving a reliable option for those looking to acquire a home. These lendings are not guaranteed or assured by the federal government, which distinguishes them from government-backed lendings. Additionally, traditional fundings may provide lower interest prices compared to FHA or VA loans, specifically for debtors with strong credit scores profiles.

In addition, FHA finances enable for higher debt-to-income ratios contrasted to traditional fundings, fitting borrowers that may have existing economic obligations. Additionally, VA loans commonly come with competitive passion prices, which can lead to reduce monthly repayments over the life of the lending.

Report this page